.webp)

.webp)

.webp)

.webp)

2024 is here, and there are significant changes to your Central Provident Fund (CPF) this year, which plays a pivotal role in your retirement planning.

From interest rate increases for certain CPF accounts to wage ceiling updates, navigating these adjustments is crucial to optimising your retirement goals.

In this article, we unpack these changes and reveal how they could affect your finances in 2024, empowering you to make informed decisions for a secure future.

5 Key CPF changes in 2024 you need to know:

- Increase in CPF Special and MediSave account interest rates

- CPF Ordinary Wage ceiling raised to $6,800

- CPF contribution rates for employees between the ages of 55 and 70 are increased

- CPF Full Retirement Sum at $205,800

- CPF Basic Healthcare Sum raised to $71,500

1. Increase in CPF Special and MediSave account interest rates

In December 2023, the CPF Board announced the interest rates for the CPF Special and MediSave account (SMA) will rise to 4.08% per annum (p.a.), up from 4.04% p.a. from 1 January 2024 to 31 March 2024.

The rate hike is attributed to an increase in the 12-month average yield of 10-year Singapore Government Securities, which the interest rate is pegged to.

The Retirement Account (RA) interest rate peg will be aligned to that of the SMA and computed quarterly instead of annually from January this year. Therefore, savings in the RA will also earn 4.08% p.a. in the first quarter of 2024.

Do take note that from 1 April to 30 June 2024, the interest rates for the SMA and RA will be 4.05% p.a..

The CPF Ordinary Account (OA) interest rate will remain unchanged at 2.5% for the same period.

Beyond the quarterly CPF interest changes, you might be interested to know that CPF members below 55 years old will earn an extra 1% interest on the first $60,000 of their combined balances (capped at $20,000 for OA).

CPF members who are 55 years old and above will also get an extra 2% p.a. interest on the first $30,000 of their combined balances (capped at $20,000 for OA), and an extra 1% p.a. on the next $30,000.

How does the change benefit you?

Simply put, the higher the interest rate, the more money you have in your CPF account at your retirement age.

For example, if you have $100,000 in your SA on 1 January 2024, this will grow to about $222,508 over 20 years based on the 4.08% p.a. interest rate, which is subject to change.

That's about $1,704 more than the $220,804 you would have in your SA after 20 years based on the previous interest rate of 4.04% p.a.

You can consider topping up your CPF SA or MA and earn up to $8,000 in tax relief. While at it, remember to top up as early as possible to maximise the growth of your CPF savings with the power of compounding!

If you top up in January each year instead of in December, you can earn up to 20% more interest on your top-ups in 10 years, based on an nterest rate of 4% p.a.. This is because your CPF interest is calculated monthly, and hence the compounding of interest begins as early as you commit your top-ups.

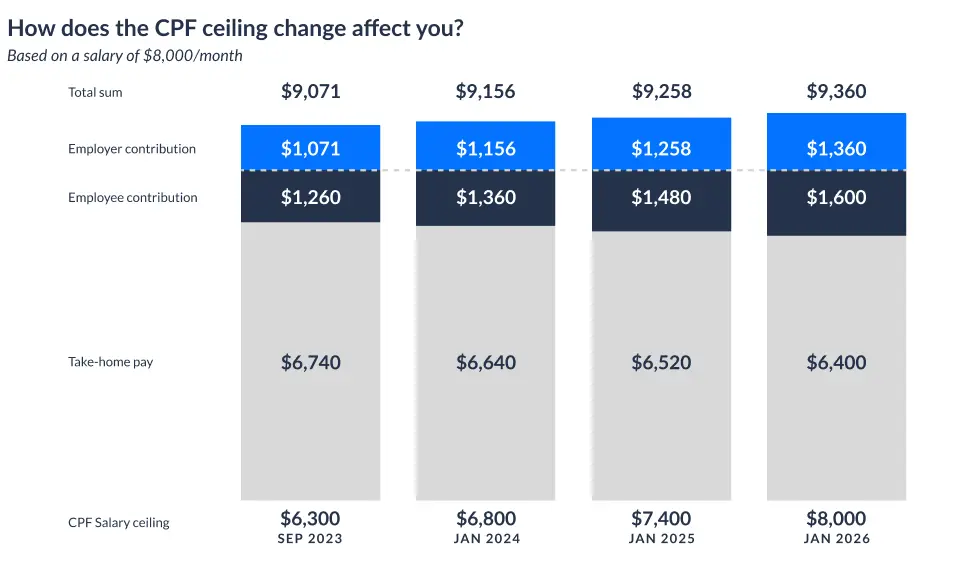

2. CPF Ordinary Wage ceiling raised to $6,800

From 1 January to 31 December 2024, the CPF Ordinary Wage (OW) ceiling will be raised from $6,300 to $6,800. The increase is progressive to allow employers and employees to adjust to the changes.

There is no change to the CPF annual salary ceiling of $102,000, which sets the maximum amount of CPF contributions payable for all salaries received in the year.

Source: CPF

How does the change benefit you?

If you earn more than $6,800 a month, your take-home pay will be lower due to the CPF monthly salary ceiling increases. This is because of the additional employee CPF contribution you must make each month.

In the short term, the decrease in your monthly take-home pay (assuming no increase in wages) can feel painful, especially if you’re the sole income earner of your household. You might need to review your personal or family finances and budget it well.

However, in the long run, your retirement savings, as a result, will grow faster than before. With a larger CPF balance, you should also be more deliberate in managing and growing your CPF, provided that the CPF OA monies have not been used for housing or education.

Do note that your employer will contribute more to your CPF as well based on the higher ceiling. If you are earning $8,000 per month, your employer will now contribute $1,360, up $100 from $1,260 at the end of 2023.

3. CPF contribution rates for employees between the ages of 55 and 70 are increased

Starting this year, the CPF contribution rates for employees between the ages of 55 and 70 will be increased, with the higher CPF contribution rates being fully allocated to the employees’ SA.

The table below shows the changes in CPF contribution rates that were announced:

How does the change benefit you?

The higher contribution rates are meant to strengthen your retirement adequacy and the full allocation of the increase to your SA will be to further increase your retirement income.

For example, if you are between the ages of 56 and 60, the allocation as a percentage of your wage to your OA, SA, and MA would be 12%, 8.5%, and 10.5% respectively. This is up from 7% to your SA before the change, with the other two allocations being the same.

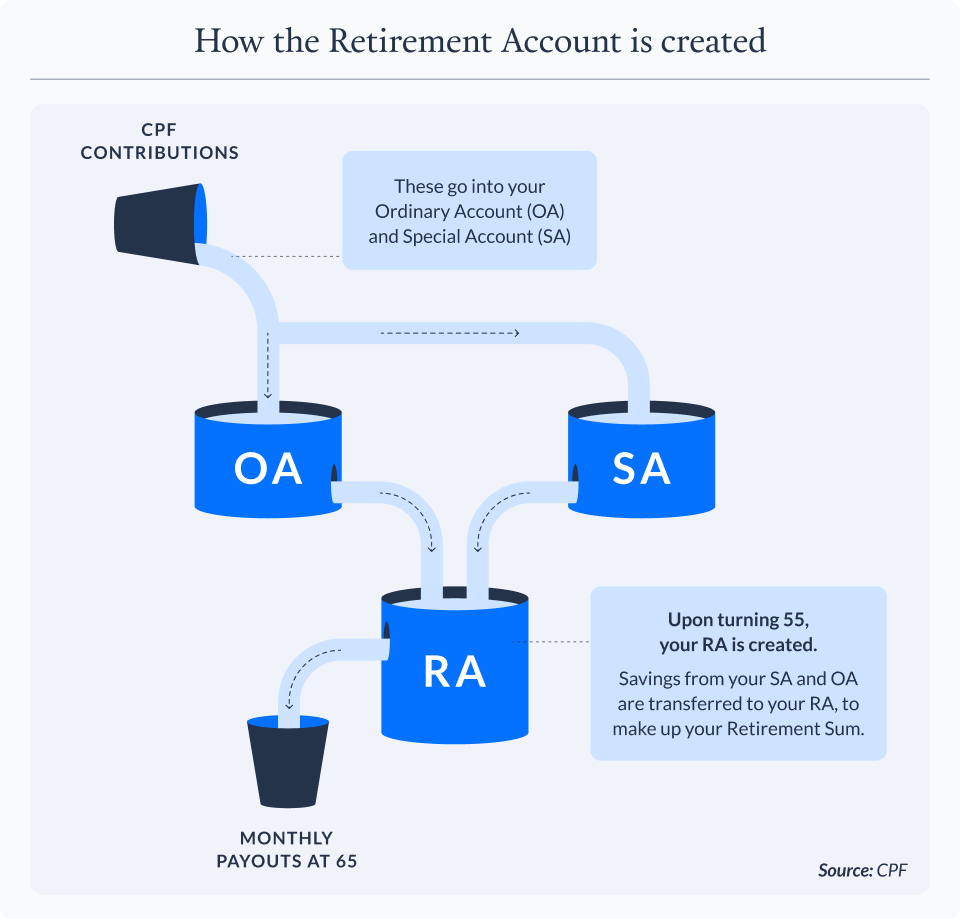

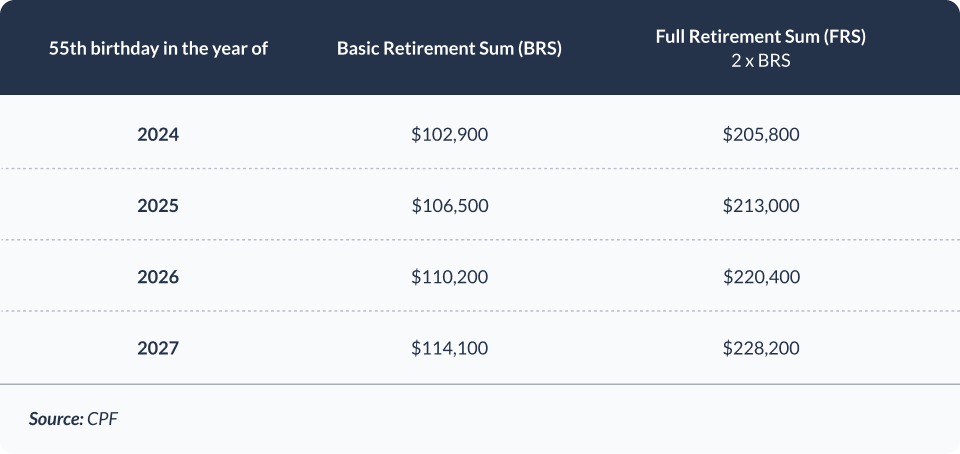

4. CPF Full Retirement Sum at $205,800

When CPF members turn 55, the RA is created, where the savings from OA and SA are transferred here.

The money in your RA will make up the different levels of retirement sums, namely, the Basic Retirement Sum (BRS), Full Retirement Sum (FRS), and Enhanced Retirement Sum (ERS).

These three levels of retirement sums attend to different personal needs:

- The Basic Retirement Sum (BRS) provides monthly payouts in retirement to cover basic living needs, excluding rental expenses.

- The Full Retirement Sum (FRS) is an ideal point of reference of how much one needs in retirement.

- The Enhanced Retirement Sum (ERS) provides a higher monthly payout, making it suitable for those who might require more retirement income.

The BRS and FRS are adjusted yearly since long-term inflation, longer life expectancy, and improvements in standard of living are taken into consideration.

In 2024, the BRS is $102,900, the FRS is two times the BRS at $205,800 and the ERS is $308,700, 1.5 times the FRS.

Read more: Using CPF and CPF LIFE for retirement

5. CPF Basic Healthcare Sum raised to $71,500

The CPF Basic Healthcare Sum (BHS) is the estimated savings you need in your MA for your basic subsidised healthcare needs during your golden years.

The BHS is adjusted annually for members below age 65 to keep pace with the growth in MediSave use. Once members reach age 65, their BHS will be fixed for the rest of their lives.

From 1 January 2024, BHS will be raised from $68,500 to $71,500 for members below 65 years old. For members who turn 65 this year, their BHS will remain at $71,500.

Taking charge of your CPF is more important now than ever

Singapore's CPF isn't just forced savings as viewed by most of us. It’s an important retirement tool.

While the interest rates in CPF are attractive, investing your CPF OA over a longer period in risk-appropriate, diversified long-term passive solutions can help you grow your CPF beyond current interest rates. The Endowus CPF Flagship Portfolio is catered for investors who are seeking higher returns with an appropriate amount of risk by accessing low-cost, highly diversified passive index funds from top-tier fund managers across a long investing horizon.

Remember, every passing moment not used to compound your money is a missed opportunity to grow your wealth.

%20(1).gif)